Our life is full of unusual and sometimes even inexplicable phenomena. Some of them...

Reimbursement of VAT from the budget is a fairly important issue that can be resolved quite simply, but with some peculiarities, the refundable amounts for payers of this tax can sometimes be significant.

To take advantage of this relief, it is necessary to calculate the tax deduction included in the reporting documentation in accordance with all the rules.

Payers related to and paying VAT, as well as those who sell goods and services subject to VAT, can take advantage of the refund.

A deduction is an amount that reduces the amount of tax contributed to the budget. For the most part, its role is played by the amount of VAT on supplier invoices; it can also be self-paid VAT, for example, the company acting as a tax agent.

Refunds are available if all conditions prescribed in Art. 171 – 172 Tax Code of the Russian Federation. It is possible to refund VAT when the amount of deductions for a tax period exceeds the amount of tax, and it is this difference that is subject to refund.

Is it possible to refund VAT and how to do it correctly you can find out in the following video:

The return is extended over quite a long time, since, first of all, the return declaration is subject to careful consideration, which is the basis of the procedure and is extended over several months. Only based on its results can you count on approval in full or in part, or receive a refusal.

To substantiate your request for a refund, you must provide evidence of arrears with appropriate documentation.

If the audit is successful, the tax office makes a decision on reimbursement and return of funds.

Important: the authority has 7 days to make a decision on these actions.

The next day after the decision is made, an order with the specified amount will be issued and sent to the Federal Treasury.

After receiving the order, the Treasury must transfer the amount to the payer’s bank account within 5 days.

Important: if the deadlines are violated and there are no funds 12 days after the completion of the desk audit, the payer will be charged interest in his favor.

If errors are detected, the following actions follow:

At the same time, according to the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation, payment of the amount is delayed and the 12-day cycle is violated only for the erroneous part. The part that does not have errors must be paid within the time prescribed by law.

What is VAT? When submitting a declaration, you should also submit an application for tax refund or credit in further calculations.

In any case, the application is submitted to the authorities at the end of the desk audit.

In case of a successful audit, the application is immediately considered; the tax authority has 12 days to do so.

The application is submitted electronically with enhanced compilation, it is accessible arbitrarily, since there is no special form, but indicating all the necessary data.

Important: if you want to return funds, indicate the bank account number, and when crediting the payment, the tax number for which the calculation should be made.

It would also be useful to clarify the tax period with the resulting arrears.

The tax office provides a response to the application in writing within 5 days directly from the head of the service or by registered mail against receipt. It will contain satisfaction of the declared amount in full or partial, or refusal.

If there is no application, then the procedure according to Art. 78 Tax Code of the Russian Federation.

To calculate VAT, you need to use a completely simple formula and step-by-step actions:

VAT allocation:

VAT calculation:

The amount must be multiplied by 1.18 or 0.18 and

VAT = S * 18 / 100., where S is the amount required for multiplication.

Example:

A known amount of 10,000 rubles at 18% then VAT will be:

Decision of the Federal Tax Service on VAT refund.

Decision of the Federal Tax Service on VAT refund. The VAT refund operation from the budget is reflected in the following when the amount is credited to the account:

If tax refunds are made against future payments, the following entries are used:

The whole procedure is not difficult, but requires extreme care on the part of the accountant responsible for making entries and drawing up documentation.

Work on returning VAT to the organization’s account consists of the following scheme:

Important: the entire required package of documents must be impeccably completed - all fields and columns must be clearly filled out, signatures, seals and details must be provided.

There are some special considerations when receiving a refund:

Enterprises that have transferred a total of several types of taxes over the last 3 years over 10 billion rubles to the budget, as well as enterprises with a bank guarantee, have the right to take advantage of the accelerated refund process.

A guarantee from a financial institution ensures that the amount is returned to the budget if the audit result is negative.

In this case, the guarantee must be more than 8 months from the date of reporting, and its amount must exceed the amount of the deduction claimed for return.

Important: the accelerated process involves the return of the declared amount before the end of the desk audit.

The application must indicate the bank account details for the transfer of funds, and indicate the security obligations in case of possible refusal. The application must be submitted within 5 days after the declaration.

The application is reviewed within 5 days from the date of receipt, as well as a check for the absence of fines and errors in the past.

After verification and if the deadlines are not met, actions occur in the same way as the standard procedure.

Mandatory and additional conditions for VAT refund from the budget are discussed in this video:

All organizations, except those that have chosen a simplified taxation system, have the right to take advantage of this deduction for VAT refunds and cost overruns.

Error-free preparation of documentation and execution of entries entirely depends on the care and skill of the accountant.

If in the VAT return for the tax period the amount of tax claimed for deduction is higher than the amount of tax calculated for payment to the budget, the taxpayer can submit an application to the tax authorities for a refund of VAT subject to reimbursement (clause 2 of Article 173 of the Tax Code of the Russian Federation). In order to reimburse VAT, an organization (or an individual entrepreneur) can show deductions in a tax return for any quarter within the 3 years established for claiming a deduction in clause 2 of Art. 173 Tax Code of the Russian Federation.

You can also submit an updated VAT return reflecting tax deductions and, subject to the specified three-year deadline, refund the tax (clause 27 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 No. 33).

Tax reimbursement from the budget is carried out on the basis of an application for VAT refund.

It must be remembered that the tax authorities will reimburse only that part of the tax claimed for deduction that is not covered by the amount of calculated VAT.

Often situations with VAT refund from the budget are related to the fact that:

If a taxpayer submits a declaration in which the amount of VAT is subject to refund, the tax authorities conduct a desk audit in accordance with the rules established by Art. 88, 100, 101 Tax Code of the Russian Federation. Based on a desk audit, tax officials make a decision on whether to refund or refuse a tax refund. The procedure and timing of VAT refunds are regulated by the provisions of Art. 176 of the Tax Code of the Russian Federation.

If a taxpayer has arrears on federal taxes or penalties and fines, then the tax authorities independently offset the amount of VAT to be reimbursed from the budget to pay off this arrears (clause 4 of Article 176 of the Tax Code of the Russian Federation).

If the taxpayer has no debt on taxes, penalties and fines, then the amount of the refunded tax can be offset against future payments for VAT and other federal taxes or returned to his current account (clause 6 of Article 176 of the Tax Code of the Russian Federation).

A taxpayer can submit an application for a VAT refund to the tax office both in writing and electronically via telecommunication channels. In the latter case, the application for VAT refund is signed with an enhanced qualified electronic signature (clause 6 of Article 176 of the Tax Code of the Russian Federation).

On our forum you can consult on any difficult issue for you regarding VAT refund. For example, we are analyzing the application procedure for VAT refund.

Order of the Federal Tax Service of the Russian Federation dated February 14, 2017 No. ММВ-7-8/182@ approved the application form for the refund of taxes, fees, insurance premiums, penalties and fines. From 01/09/2019, this form is used as amended by the Federal Tax Service order dated 11/30/2018 No. ММВ-7-8/670@.

On our website you can download this application form and view a completed sample.

A letter to offset the overpayment to the supplier is very useful if, under any agreement with a counterparty, there is a larger difference in payment for services or goods.

FILES

Overpayment between counterparties can occur for a number of reasons:

Before drawing up a letter about the offset of the overpayment, you need to make sure that the calculations by the organization’s accounting department were made correctly. To do this, the supplier is asked to draw up a bilateral reconciliation report. This will allow you to reach a common opinion regarding the amount of the overpayment.

Typically, this kind of paper is printed on the organization’s letterhead. On their upper part are the company details. If a business letter is printed on a regular A4 sheet without notes, then at the very top you must indicate the name and basic information of the organization that is sending the message.

The letter must contain:

If an overpayment occurs, there are two options: a refund or offset against other agreements. Sending an overpayment offset letter to a supplier involves the first option, so it should be specific about what action is expected of the supplier.

The supplier may agree to the terms proposed in the letter, or may refuse them. Also, if you refuse, he will probably offer his own way out of the situation. For example, it will be much more convenient for the supplier’s accounting department (and more profitable for their manager) to transfer excess funds back than to transfer them towards future deliveries.

The likelihood of such circumstances is especially increased by the lack of information on this point in the contract between organizations. Thus, the supplier may have to provide another letter requesting a refund of the overpaid funds.

If an incorrect payment (for goods not delivered, services not performed, etc.) was provided along with VAT, then the amount of this payment should be recalculated. The algorithm is as follows:

However, there is a fundamentally important nuance regarding the last point. The amount that was overpaid is, in fact, an advance payment for future delivery. However, VAT should not be taken from it until the shipment or provision of services. After all, the contract (referenced by the correct invoice) indicates a different contract number with the supplier. And before the transaction is actually completed, the deduction will be illegal.

In the letter about offset of the overpayment to the supplier, be sure to specify under which specific agreement the overpayment arose and in what amount.

At the same time, indicate what you expect from the seller. For example, so that he can offset other agreements. Provide the number and date of the contract to which you are asking to transfer the overpayment. It is better to put live signatures and stamps on the document, send it by mail or deliver it with a courier. There are no trifles in business correspondence.

If the supplier somehow failed to fulfill his obligations (the delivery of the goods was not complete, there was inadequate quality, an unacceptable delay, etc.), then one letter about the offset of the overpayment to the supplier will not be enough. The organization will have to change the terms of the existing contract or terminate it altogether.

All business correspondence must go through the outgoing documentation journal. It notes the main content of the letter, its number and date. This way you can confirm the existence of the paper if legal proceedings are subsequently held on this issue.

As for the storage period, for letters of this kind it is 5 years.

This is due to the fact that it is directly related to the business relationship with the supplier of goods or services. When these documents, the letter of request and the letter are systematized, the response to it is classified as a single matter. This is the only way to reconstruct the entire course of the correspondence and study the arguments and demands of both sides subsequently.

If the amount of tax deductions exceeds the calculated amount of VAT, the “input” VAT is subject to reimbursement in the manner and within the time limits established by Art. 176 of the Tax Code of the Russian Federation (clause 2 of Article 173 of the Tax Code of the Russian Federation).

If there is a written application from the taxpayer, the amounts to be refunded may be directed towards payment of upcoming tax payments or other federal taxes (clause 6 of Article 176 of the Tax Code of the Russian Federation). Simultaneously with the decision on reimbursement (full or partial) of tax amounts, the tax authority makes a decision on offset or refund of tax (clause 7 of Article 176 of the Tax Code of the Russian Federation).

If the application for offset is not submitted by the taxpayer before the date of the decision on tax refund (in whole or in part), offset (refund) of the tax amount is made in the manner and within the time limits established by Art. 78 of the Tax Code of the Russian Federation (clause 11.1 of Article 176 of the Tax Code of the Russian Federation).

On the issue of reflecting the operation of offsetting a tax calculated for reimbursement from the budget against upcoming payments for the same tax, there are two positions: the first is not to reflect the operation, the second is to reflect it on the corresponding second-order subaccounts. The most “informative” is position 2, since it allows you to see what amount was offset against upcoming payments for the same tax, but everyone has the right to be guided by their professional judgment when choosing an action option.

Position 1. On the basis that the debt to the budget does not change, the offset operation is not reflected in accounting, and in the next tax period the amount of tax accrued for payment on the basis of the declaration will be reduced by the taxpayer by the amount of overpayment for this tax.

Based on the VAT return for the first quarter of 2014, the amount of tax calculated for reimbursement amounted to 100,000 rubles. The company submitted an application to the tax authority to offset the said amount against upcoming payments for this tax. The tax authority made a corresponding decision.

For the second quarter of 2014, according to the declaration, the amount of tax payable was 500,000 rubles.

|

Amount, rub. |

|||||||||||||||||||||||||||

|

VAT paid for the second quarter of 2014 |

— 68-2-1 “Calculations for VAT”; — 68-2-2 "Calculations for VAT offset against future tax payments." Let's use the conditions of example 1. The correspondence of invoices will be as follows:

The enterprise offset the VAT calculated for reimbursement from the budget against future tax payments. How to reflect this transaction in accounting? In 2019, the documents that legal entities and individuals must use to offset and return overpayments of taxes have changed. Let's look at what the application form for offset of overpayment of tax now looks like and how to fill out this document correctly. Application forms used to offset and return amounts of overpaid (collected) taxes, fees, insurance premiums, penalties, and fines were approved by Order of the Federal Tax Service dated February 14, 2017 No. ММВ-7-8/. They should be used by both individuals and legal entities. But since 2019, small changes have been made to the Federal Tax Service order, which must be remembered. When will new forms be needed?According to Article 78 of the Tax Code of the Russian Federation, taxpayers who have overpaid can dispose of the overpaid amounts in different ways:

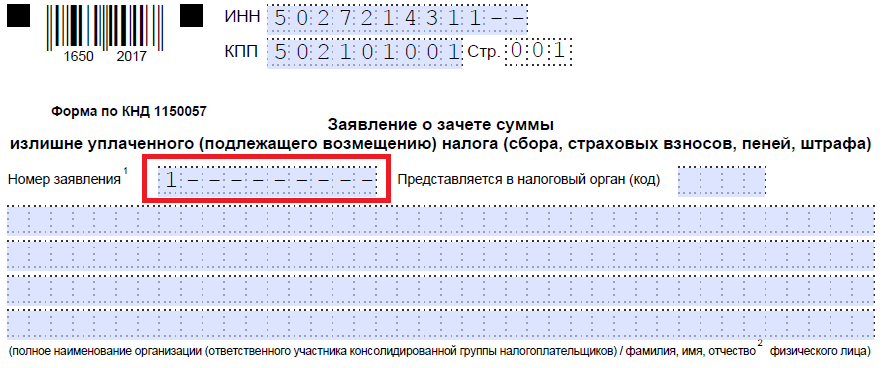

These rules apply to all fees and taxes introduced in the Russian Federation, including state duty (with some features listed in Article 333.40 of the Tax Code of the Russian Federation), VAT, advance payments. However, you must understand that the tax service will not return or offset the overpaid amount against future payments until the debt is paid off. Sample application for offset of overpaid taxIf the taxpayer decides to reallocate his money, he needs to write a tax offset application. The form of this document is presented in the order of the Federal Tax Service from application No. 9. You can download it at the bottom of the page. How to fill out such a documentLet's say Kolosok LLC filed a transport tax return for 2018, but when paying it made a mistake, paying 3,112 rubles more. The organization applies to the interdistrict Federal Tax Service and asks for a credit for the overpayment of taxes; she writes in order to have the overpaid amount credited to her upcoming corporate property tax payments. Let's look at filling out such a document step by step. Step 1. Traditionally, the TIN and KPP should be indicated at the very top. The individual entrepreneur’s identification number consists of 12 digits, so there should be no free cells left. Organizations enter only 10 numbers in the appropriate fields, and put dashes in the remaining two. When filling out the line intended for the checkpoint, applicants must act in the same way: if there are numbers, enter them, if not, put dashes. Step 2. Enter the request number. Here they put down the number of times in the current year they applied for the test. Don’t forget about dashes if the number of numbers to be entered is less than the number of cells.

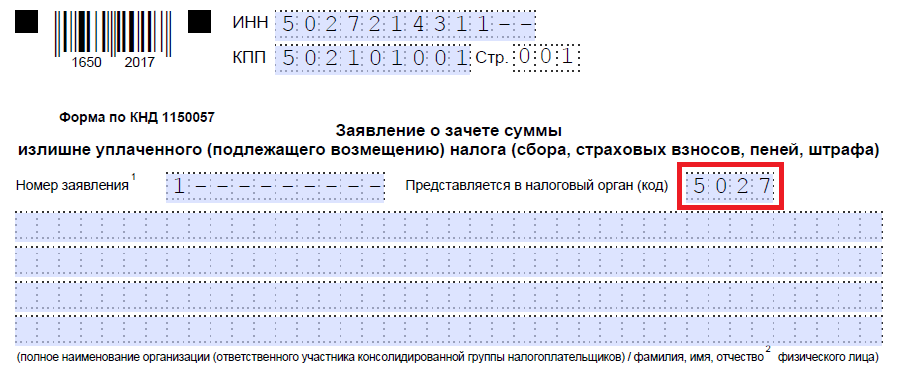

Step 3. Enter the code of the tax authority where the application will be sent. This should be an inspection of the Federal Tax Service at the place of registration of the individual entrepreneur or organization. In a consolidated group of taxpayers, the responsible member of this group must request a credit for the overpayment of income tax.

Step 4. We write down the full name of the applicant organization, for example, limited liability company “Kolosok”. Fill in the remaining cells with dashes. None of them should be left empty. When filling out this field by an individual entrepreneur, he must indicate his last name, first name and patronymic, if any. In addition, the status of the applicant, as whom he is applying, should be indicated in accordance with the instructions:

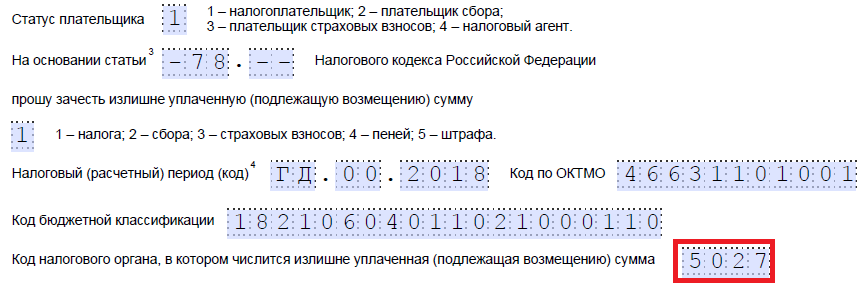

Step 5. We indicate the article of the Tax Code of the Russian Federation, on the basis of which the offset can be made. It will depend on which payment was overpaid. The Federal Tax Service left 5 cells to indicate a specific article. If some of them are not needed, dashes must be added. Here are the options for filling out this field:

Step 6. We write down what exactly the overpayment was for - taxes, fees, insurance premiums, penalties, fines.

Step 7. The applicant specifies for what period the overpayment occurred. The developers provided 10 familiar places to indicate the code, of which two are dots. The first two of them can be filled in with one of the following options:

Specific values will depend on the reporting period provided for by law for the payment for which offset is planned. In the 4th and 5th acquaintances, the reporting period is specified:

The last four familiar places are intended to indicate a specific year, for example 2019. Instead of alphanumeric combinations, a specific date can be recorded, for example 01/25/2019. Such an entry is permitted if the legislation provides for a specific date for paying the fee or submitting a declaration. Examples of filling out the billing period: “MS.02.2019”, “KV.03.2019”, “PL.01.2019”, “GD.00.2019”, “04.05.2019”.

Step 8. Enter the OKTMO code. If you don’t know it or have forgotten it, you can call the Federal Tax Service at the place of registration or go to nalog.ru to find out the required code by the name of the municipality.

Step 9. We accurately enter the KBK for payment of the corresponding payment, using Order of the Ministry of Finance of Russia dated 06/08/2018 N 132n. You can also find out the code using the Federal Tax Service website or look at it on a previously completed payment order.

Step 10. We clarify to which Federal Tax Service the excess funds were transferred.

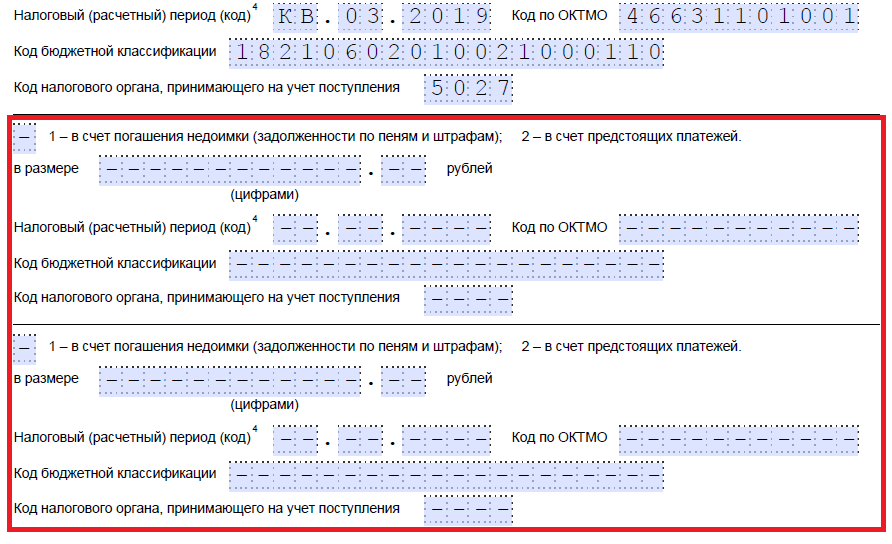

Step 11. On the first sheet, it remains to fill in how many sheets the application is submitted on and how many sheets of supporting documents are attached, as well as indicate information about the applicant himself. We recommend leaving these two small sections for later. Let's continue filling on the second sheet. In the very first field where you need to indicate your last name, first name and patronymic, put dashes. Below we indicate what needs to be done with the overpayment - pay off the debt or leave funds for upcoming payments.

Step 12. We write down the specific amount that the applicant wants to offset. It is indicated in numbers, without text decoding.

Step 13. We fill in the period for the payment for which we plan to offset. In our case, the corporate property tax is quarterly, so we enter the quarter in which the overpayment should go.

Step 14. Write down the OKTMO code again. As a rule, it is duplicated.

Step 15. We specify the KBK for the transfer of funds, into which the excess amount will go. Ours is different from the previous KBK, since the taxes are different. If the overpayment goes towards future payments for the same fee, then the BCCs are the same. An exception is if the codes were previously changed by decision of the Ministry of Finance. Let us also recall that offsets can be carried out according to certain rules: they must relate to the same type: federal, regional or local. For example, it is not possible to offset the federal portion of the income tax against upcoming trade tax payments.

Step 16. The code of the Federal Tax Service, which accepts receipts, is usually duplicated.

Step 17. Since there are no more overpayments, in our example the following lines are not filled in. You can put spaces there. Also, organizations and individual entrepreneurs do not fill out the third sheet. It is intended for individuals who are not registered as individual entrepreneurs and who have not indicated their TIN.

Step 18. Return to the first sheet and enter the number of pages and attachments. Applicants indicate the relevant data in the provided fields.

Step 19. The last part of the application should not cause problems when filling out. Here you need to clarify who is submitting the appeal and when, as well as indicate a contact phone number. The right side remains blank: it is intended for marks from Federal Tax Service inspectors.

How to get your money backIf an entrepreneur (company) decides to return the overpayment amount, he needs to use another form from the Federal Tax Service order dated February 14, 2017 No. ММВ-7-8/, proposed in Appendix No. 8. It contains a form for returning the excess amount. The rules for filling out this document are approximately the same. Therefore, we will not consider them in detail, but will give an example of a completed document. Let’s say Kolosok LLC overpaid VAT for the first quarter of 2019 in the amount of 15,732 rubles and now wants to return it. This is what an appeal from the head of an LLC will look like. When and how to submit an appealAccording to Article 78 of the Tax Code of the Russian Federation, you can apply for credit and refund within 3 years from the date of payment of the fee. There are three ways to deliver documents:

Having received such an application, the tax authority decides whether to satisfy it or not. The service notifies the entrepreneur of its decision within 10 days from the date of receipt of the application. As a rule, if the initiative comes from an organization or individual entrepreneur, the Federal Tax Service does a reconciliation of the calculations. If the inspector himself discovers the overpayment, the reconciliation may be refused. The entrepreneur is not relieved of the obligation to submit an application. We recommend reading

Our life is full of unusual and sometimes even inexplicable phenomena. Some of them...

Choose a name according to the horoscope: Capricorn What male name is suitable for a Capricorn woman

Compatibility horoscope: Capricorn zodiac sign, what names are the most complete...

|